Did you know SARS reduces your tax bill every month you’re on medical aid? Most South African families don’t, and the ones who do often aren’t claiming it correctly. It’s called the medical aid tax credit, and for a family of four, it’s worth R14,640 a year.

It applies to the principal member, their spouse, and all registered dependants. Your income doesn’t affect your eligibility. And it’s separate from the Additional Medical Expenses Tax Credit, which covers qualifying out-of-pocket costs your scheme doesn’t pay for.

Here’s how it works for the 2026 tax season.

What’s the medical aid tax credit?

Each month you’re on a registered medical scheme, SARS knocks a fixed amount off your tax bill. That’s the Medical Tax Credit, Section 6A of the Income Tax Act, for the record. It’s not a deduction. Deductions reduce your taxable income before the number is worked out. This reduces the number itself. For most families, that difference translates into real money. That makes it more valuable, rand for rand, particularly for families in middle-income brackets.

The credit was put in place to bring down the effective cost of medical aid membership.

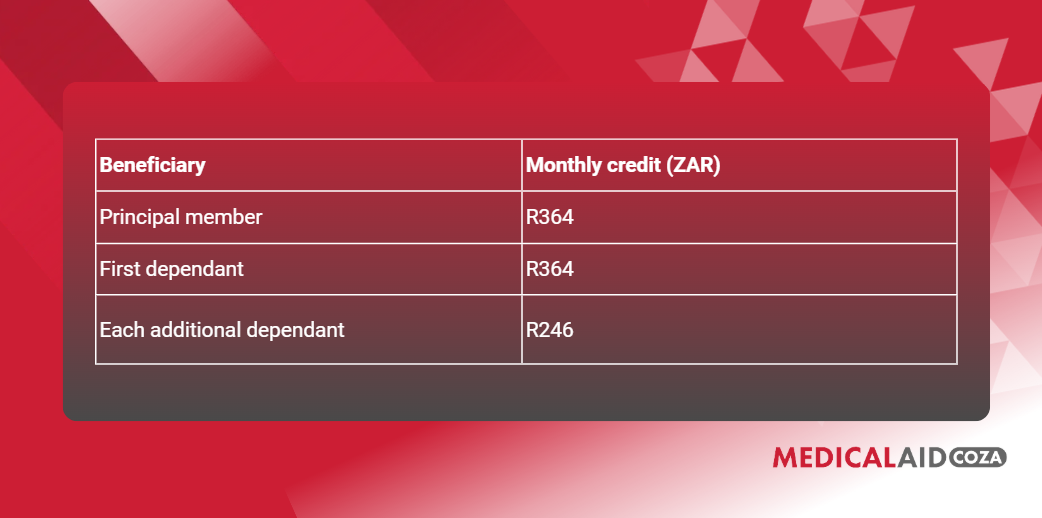

How much is the credit worth in 2026?

SARS sets the medical aid tax credit 2026 amounts annually. For the 2026 tax year (1 March 2025 to 28 February 2026), the applicable amounts are:

A family of four (two adults, two children) receives a combined monthly credit of R1,220, or R14,640 over the full tax year.

Always verify the latest figures directly with SARS or your tax practitioner, as these amounts are subject to annual revision.

How does it reduce your tax bill?

The credit is applied after your income tax liability has been calculated. It is subtracted directly from what you owe SARS, not from your income before the calculation.

Worked example for a family of four:

| Calculated tax liability | R42,000 |

| Annual MTC (family of four) | R14,640 |

| Tax payable after credit | R27,360 |

R14,640 back in your pocket. For a household carrying medical aid contributions on top of school fees and groceries, that’s not a small number.

How do you claim the medical aid tax credit?

For most employed South Africans, the process is largely automatic. Here is how to claim medical aid tax credit correctly:

- Your employer deducts your medical aid contributions from your salary each month.

- The MTC is factored into your PAYE calculation by your employer’s payroll system, reducing your monthly tax deduction.

- At tax filing time, you declare your contributions on your ITR12 return.

- SARS calculates and applies the credit automatically based on the number of registered beneficiaries on your plan.

- If you are self-employed, you claim the credit manually when submitting your annual return.

When filing your ITR12 medical aid credit section, have your annual contribution certificate ready. Your scheme issues this after the tax year ends. It confirms the total contributions paid and the number of registered dependants.

Does your plan affect what you can claim?

The MTC amount is fixed regardless of which medical aid plan you are on. However, the plan you choose does affect your total out-of-pocket healthcare costs, and that matters when it comes to a second credit.

The Additional Medical Expenses Tax Credit (AMTC) allows qualifying taxpayers to claim a portion of medical expenses not covered by their scheme. This applies mainly to South Africans aged 65 and over, or those with a disability, whose qualifying out-of-pocket expenses exceed a set threshold.

For families under 65 without a disability, the MTC is where the focus sits. A plan with a low monthly contribution sounds good until you add up what you’re spending at the doctor, pharmacy, and hospital. Are you sure your current plan is giving your household value? You can read more in our guide, Does your current medical aid still fit your needs?, or compare options directly on MedicalAid.co.za.

View medical aid options on MedicalAid.co.za to see how plans differ based on your household size and budget.

Frequently asked questions

Is the medical aid tax credit the same as a tax deduction?

No. A deduction reduces your taxable income before your tax is worked out. A tax credit reduces your actual tax liability after the calculation. Credits are generally more valuable because they reduce your bill rand for rand, regardless of your tax bracket.

What’s the difference between the MTC and the SARS medical aid rebate?

They’re the same thing. The SARS medical aid rebate is the name that was used before the system was formalised as the Medical Tax Credit under Section 6A. Both refer to the fixed monthly credit applied to your tax liability for contributions to a registered scheme.

What if my employer pays part of my medical aid?

The MTC applies to the full contribution, regardless of who pays it. However, the portion paid by your employer is treated as a fringe benefit for tax purposes. Speak to a tax practitioner if you are unsure how this affects your overall return.

Can I claim for dependants who are no longer on my plan?

No. The credit only applies to registered dependants for the months they were active on your plan. If a dependant was removed mid-year, the credit applies only for the period they were covered.

Find a plan that works harder for your family

The medical aid tax credit exists to reduce what your family pays. But it works alongside your plan, and if your plan isn’t the right fit for your household’s needs and budget, you’re not getting the full picture. When last did you compare your options? Families at different life stages often find the numbers look different when they sit down and check. If someone in your household is newer to medical aid, our guide on what young professionals should compare before joining is worth a read, too.

Compare medical aid options on MedicalAid.co.za and see which plans give your household the best combination of cover and value.