“My plan is active, so why did I still pay?” is not a new question to South Africans. You pay your medical aid every month… so why does a bill still land in your inbox?

If you have ever asked that after a doctor visit, scan, or hospital visit, you’re not alone. Many South African medical schemes use provider networks to manage costs and agree on rates. That’s where Designated Service Providers (DSPs) come in.

This guide explains how DSP and network rules typically work, when extra costs may apply if you go out of network, and what to check before you claim.

In most situations, “out of network” doesn’t mean your claim will automatically be rejected. Instead, different rules may apply. For example, there could be a co-payment, a payment limited to the scheme rate, or additional steps like pre-authorisation.

You’ll also find a simple checklist to use when comparing options. That way, you can spot network rules that may matter most to you or your household.

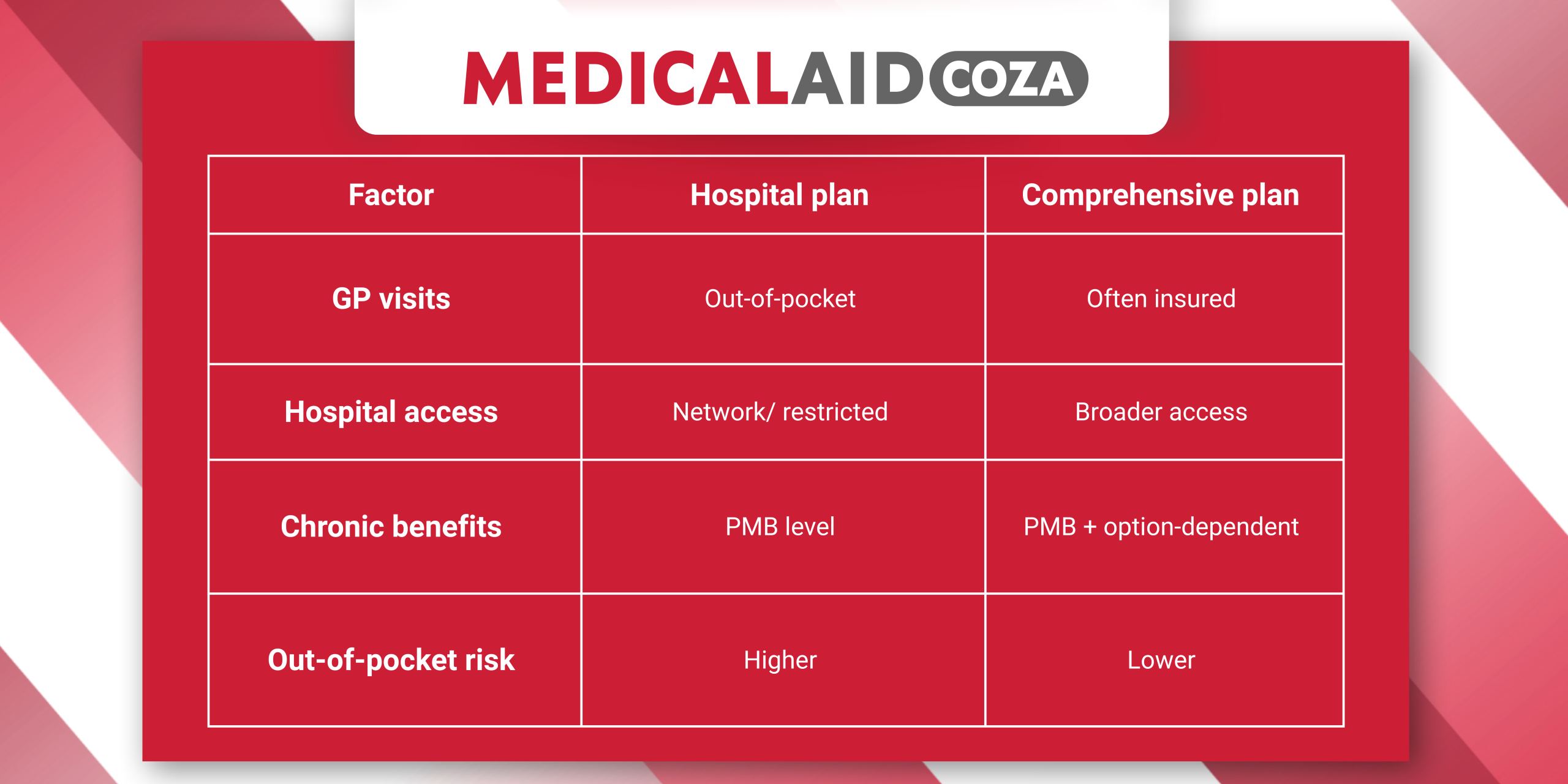

View options to compare the benefits of different medical aids side-by-side before you choose.

What is a DSP in South African medical schemes?

A Designated Service provider (DSP) is a healthcare provider, or group of providers, that has a contract with a medical scheme and is listed in the scheme rules as a preferred provider for certain services.

Your option may guide you toward certain hospitals, doctors, pharmacies, or service providers for services like scans or blood tests. Importantly, whether a provider is “in network” may depend on the specific service you need, not only the provider itself.

DSP vs network provider

You may notice that “DSP” and “network provider” are often used interchangeably in member communication. Some schemes use “network” as the easier term, while “DSP” usually appears in official benefit documents and option rules.

Either way, the practical point remains the same: If your option lists preferred providers for a service, using someone outside that list may change how the claim is paid.

What does “out of network” mean in practice?

When people hear “out of network”, they often think of hospitals first. But network rules can apply to many types of healthcare services.

Depending on your option, this may include:

- GPs and specialists

- Pharmacies (including repeat medicine)

- Pathology and radiology (blood tests, MRI, CT)

- Referral pathways and authorisation steps

Because networks differ by scheme and option, two people can be on the same scheme and still have different network rules.

Why schemes use networks

Networks help schemes agree on rates and billing processes with specific providers. They also support more predictable care pathways for certain services. Many options use tools like pre-authorisation, protocols, and formularies to guide how care is accessed and paid, especially where costs can escalate quickly.

How going out of network can cost you more

3 common cost outcomes

Going outside your option’s network doesn’t always mean a claim won’t be paid. However, different cost outcomes may apply depending on the scheme rules. Some of these outcomes include the fact that:

1) Co-payments may apply

If your option rules require a DSP or network provider for a service, choosing a non-network provider may trigger a co-payment.

Example: Your option requires a network radiology group for MRI scans. If you book at a non-network practice, a co-payment may be charged, depending on your rules.

2) The scheme pays up to a set rate, and you pay the difference

Many services are reimbursed at a scheme rate (scheme tariff). If a provider charges above that rate, you pay the balance.

Example: A specialist charges above scheme rate. Your scheme pays up to the allowed rate on your option, and the difference may be for your own account. This is sometimes called balance billing.

3) A claim may be reduced if rules aren’t followed

Some options require certain steps before treatment takes place. If these steps aren’t followed, benefits may be affected.

Example: A planned hospital admission may require pre-authorisation. If authorisation isn’t obtained, the claim may be reduced, or a co-payment may apply depending on the rules.

These outcomes aren’t automatic. The exact detail always depends on the scheme rules. But knowing the common triggers beforehand can help you avoid unexpected costs.

View options to see how different options handle network rules, scheme rates, and common co-payment triggers.

Where people get caught out most often

If you’re new to medical schemes, it helps to know that network rules usually appear in everyday healthcare moments, not only during major events. These are situations where members are often surprised by extra costs. Some of these situations include:

Planned scans and diagnostics

MRI scans, CT scans, specialised blood tests, and radiology services are often linked to preferred provider networks. If you use a provider outside the network, the claim may be paid differently.

Specialist visits

Specialists sometimes charge above scheme rate. In addition, some options require referrals or specific pathways before specialist consultations are covered fully.

Hospital admissions

Hospital networks can be strict. Your option may only include certain hospital groups or apply different rules if you choose a non-network hospital for planned procedures.

Medicine and pharmacy choice

Some options require members to use preferred pharmacies or follow a medicine formulary. If scripts are filled outside those rules, benefits may be paid differently.

So, the simplest way to avoid surprises? Check the rule before you book, not after the claim is processed.

Quick checklist: what to check before you book a procedure or get admitted.

Before committing to a provider or procedure, it helps to run through a few key questions:

- Is this provider in-network for my option and for this service?

- Do I need pre-authorisation?

- Do I need a referral to see a specialist?

- Are there protocol or formulary requirements for this service or condition?

- What co-payments are listed in the option rules for out of network use?

- What rate does the scheme pay for this service, and what may be for my account if the provider charges above that rate?

How to compare options on Medicalaid.co.za

When comparing medical aid options, it helps to look beyond the premium. Instead, focus on how each option handles network rules and claims processes.

Here are five things worth comparing:

- Network and DSP requirements (hospital, pharmacy, day-to-day providers).

- Authorisation and referral rules (what needs approval and when).

- Co-payment triggers (especially out-of-network rules).

- Scheme rates and how provider charges are handled.

- How clearly the option explains benefits and member responsibilities.

If you’d like to understand these topics in more detail, explore the explainers on the Medicalaid.co.za news page. They cover some of the most common medical aid questions South Africans ask.

View options as the next step for early-stage research, so you can compare medical aids side by side before choosing the one that is best for you.